Introduction

When it comes to home financing, veterans and active-duty service members have a distinct advantage through VA loans. These loans, backed by the U.S. Department of Veterans Affairs, offer numerous benefits that make homeownership more accessible and affordable for those who have served their country.

In this article, we’ll delve into the advantages of VA loans and how they empower military personnel and their families to achieve their homeownership dreams. However, like other things, these loans also have their disadvantages, and we will look at those too.

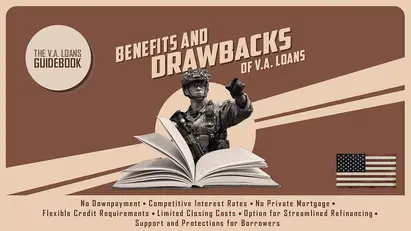

The Benefits

Here are some of the benefits offered by VA loans to those who qualify for them.

-

No Down Payment Requirement: One of the most significant advantages of VA loans is that they typically do not require a down payment. For many prospective homebuyers, scraping together a substantial down payment can be a significant barrier to homeownership. However, VA loans eliminate this obstacle, allowing qualified borrowers to purchase a home with little to no money down. This feature opens opportunities for veterans and active-duty personnel to invest in homeownership sooner rather than later, without having to save for years to accumulate a large down payment.

-

Competitive Interest Rates: VA loans often come with competitive interest rates, which can result in substantial savings over the life of the loan. The Department of Veterans Affairs guarantees a portion of the loan, making lenders more willing to offer favorable terms to eligible borrowers. With lower interest rates, veterans can enjoy more affordable monthly mortgage payments, freeing up funds for other essential expenses or savings goals. This aspect of VA loans reflects the government’s commitment to supporting veterans and military families in achieving financial stability.

-

No Private Mortgage Insurance (PMI): Unlike conventional loans, VA loans do not require private mortgage insurance (PMI), even with a zero down payment. PMI is typically mandatory for borrowers who put down less than 20% on a conventional loan and serves to protect the lender in case of default. By eliminating the need for PMI, VA loans can save borrowers hundreds of dollars each month, further enhancing affordability and making homeownership more attainable for those on a tight budget.

-

Flexible Credit Requirements: While traditional mortgage lenders often have strict credit score requirements, VA loans tend to be more flexible in this regard. Although the VA itself doesn’t set a minimum credit score requirement, most lenders look for a credit score of around 620 or higher. Additionally, VA loans consider the borrower’s entire financial profile, including income, assets, and debt-to-income ratio, rather than solely relying on credit scores. This flexibility means that veterans with less-than-perfect credit histories still have a chance to qualify for a VA loan and fulfill their homeownership aspirations.

-

Limited Closing Costs: VA loans come with restrictions on certain closing costs, further reducing the financial burden on borrowers. The VA regulates the fees that veterans can be charged, limiting what lenders can charge for origination fees, appraisal fees, and other closing costs. Additionally, sellers can contribute towards the buyer’s closing costs, which can result in even more savings for the veteran. By minimizing closing costs, VA loans make it easier for veterans to transition into homeownership without being overwhelmed by upfront expenses.

-

Option for Streamlined Refinancing (IRRRL): For veterans who already have a VA loan, the Interest Rate Reduction Refinance Loan (IRRRL), also known as the VA Streamline Refinance, offers a hassle-free way to lower monthly mortgage payments. With an IRRRL, borrowers can refinance their existing VA loan to obtain a lower interest rate without the need for a new appraisal or extensive paperwork. This streamlined process can result in significant savings over time, providing veterans with more financial flexibility and stability.

-

Support and Protections for Borrowers: VA loans come with built-in protections for borrowers, ensuring that veterans are treated fairly throughout the homebuying process. The VA oversees the administration of these loans, setting standards for lenders and providing recourse for borrowers in case of disputes or issues. Additionally, VA loans help programs for veterans facing financial hardship, such as repayment plans and loan modification options, further demonstrating the government’s commitment to serving those who have served their country.

VA loans offer many benefits that make homeownership more accessible and affordable for veterans and active-duty service members. From no down payment requirements to competitive interest rates and limited closing costs, VA loans empower military personnel and their families to achieve the American dream of owning a home. Moreover, the flexibility and support provided through VA loans reflect the nation’s gratitude for the sacrifices made by those who have served in uniform.

The Drawbacks

Like any financial product, VA loans come with their own set of drawbacks and limitations that borrowers should be aware of before diving in. It’s important to explore some of the potential downsides of VA loans to help borrowers make informed decisions.

-

Funding Fee: One of the notable drawbacks of VA loans is the funding fee. While VA loans typically don’t require a down payment, borrowers are often required to pay a funding fee, which helps offset the cost of the loan to taxpayers since VA loans are backed by the government. The VA funding fee is a one-time fee paid to the Department of Veterans Affairs and it can vary depending on factors such as the type of service (regular military, National Guard, or Reserves) and whether it’s the borrower’s first VA loan or subsequent usage. Although this fee can be rolled into the loan amount, it still adds to the overall cost of homeownership and can be a significant expense for some borrowers.

-

Property Eligibility: Another limitation of VA loans is the property eligibility requirements. While VA loans can be used to finance various types of properties, including single-family homes, condominiums, and multi-unit properties, they must meet certain standards set by the VA. These standards include minimum property requirements (MPRs) to ensure the home is safe, structurally sound, and sanitary. Properties that do not meet these requirements may not be eligible for VA financing, limiting the options available to borrowers, especially in competitive housing markets.

-

Appraisal Process: The VA requires an appraisal for every home financed with a VA loan to determine its value and ensure it meets the minimum property requirements. While appraisals are standard practice in the homebuying process, the VA appraisal process can sometimes be more stringent compared to conventional appraisals. If the appraisal comes in lower than the agreed-upon purchase price, it can create challenges for the borrower, such as renegotiating the price with the seller or covering the shortfall out of pocket. Additionally, delays in the VA appraisal process can prolong the homebuying timeline, which may not be ideal for borrowers with strict deadlines.

-

Occupancy Requirement: VA loans are intended to help eligible borrowers purchase a primary residence. As such, there’s a strict occupancy requirement that borrowers must fulfill. Borrowers are expected to occupy the property as their primary residence within a reasonable time frame after closing on the loan. While this requirement aligns with the VA’s mission to promote homeownership among veterans and service members, it may not be feasible for borrowers who have plans to relocate or invest in rental properties. Violating the occupancy requirement could have serious consequences, including the possibility of the VA demanding immediate repayment of the loan.

-

Entitlement Limitations: VA loans come with entitlement limitations, which dictate the maximum amount the VA will guarantee for each eligible borrower. The entitlement is typically enough to finance a home purchase up to a certain loan limit set by the VA. However, borrowers who have previously used their VA loan benefit and still have an outstanding VA loan balance may have limited remaining entitlement, which could affect their ability to secure another VA loan without a down payment. This limitation can be particularly challenging for borrowers in high-cost housing markets where home prices exceed the VA loan limits.

-

Funding Delays: While VA loans offer many benefits, the loan process can sometimes be slower compared to conventional loans. Due to the VA’s involvement in the loan approval process and the additional requirements such as VA appraisals and underwriting guidelines, funding delays are not uncommon. For borrowers in competitive real estate markets where timing is crucial, such delays could result in losing out on a desired property or facing increased pressure to close quickly, potentially leading to added stress and uncertainty.

While VA loans provide valuable opportunities for eligible service members, veterans, and their families to achieve homeownership with favorable terms, it’s essential to understand and consider the potential drawbacks before committing to this type of loan. From funding fees and property eligibility requirements to occupancy limitations and funding delays, there are various factors that borrowers need to weigh carefully.

By being aware of these drawbacks and seeking guidance from knowledgeable professionals, borrowers can make informed decisions that align with their financial goals and circumstances. Ultimately, while VA loans can be a valuable tool for achieving the dream of homeownership, it’s crucial to approach them with a clear understanding of both their benefits and limitations.